AI and the climate transition: two engines of economic growth despite geopolitical pressures

Koen De Leus, Chief Economist, and Philippe Gijsels, Chief Strategist, both of BNP Paribas Fortis, expect the economic and financial environment to continue to be shaped by geopolitical tensions. This will result in persistent inflationary pressures and higher interest rates. While this weighs on growth, it also creates new opportunities. In the long term, they see artificial intelligence as a key driver of productivity and economic growth. At the same time, despite its short-term costs, an accelerated climate transition could generate significant economic benefits. For Belgium, however, weak public finances and rising long-term interest rates remain major concerns. Against this backdrop, the economists continue to adopt a positive long-term outlook on equities, emphasise the strategic importance of commodities, and favour high-quality bonds with medium-term maturities.

Slideshow Midyear Economic & Investment Outlook 2026.pdf

PDF 14 MB

Part I: macroeconomic overview

Recent tensions in the Middle East have created significant uncertainty in the energy market. Disruptions to key trade routes are pushing oil and gas prices up. Consequently, almost 15% of global oil output is currently unable to reach the market. Rising energy prices are already being felt by consumers. High fertiliser prices are also expected to push up food prices in the coming months. Furthermore, a large majority of European and Belgian manufacturers in the industrial and construction sectors have indicated their intention to raise prices over the next three months. If the Strait of Hormuz remains closed in the months ahead, physical shortages could emerge, leading to further sharp price increases.

Economic figures

Belgium

At the beginning of this year, BNP Paribas Fortis estimated Belgian economic growth at 1.1% by the end of 2026. However, the bank has since revised this figure downwards, forecasting growth of just 0.7% by the end of this year, rising to 0,9% by the end of 2027. Inflation is expected to average 3.5% in 2026 and 2.2% in 2027.

Eurozone

BNP Paribas Fortis forecasts growth of 0.6% in the eurozone by the end of 2026 and 1.6% by the end of 2027. Inflation is expected to reach 3.0% and 3.3%, respectively. The bank expects the European Central Bank to raise its policy rate from 2.0% to 2.5% by the end of 2026, maintaining this level until the end of 2027.

United States

In the United States, BNP Paribas Fortis forecasts growth of 2.3% by the end of 2026 and 2.4% by the end of 2027. Inflation is expected to reach 3.7% by the end of 2026 and 2.8% by the end of 2027. The Federal Reserve’s policy rate is expected to remain stable at 3.75% until the end of 2026. The bank expects the policy rate to reach 4.5% by the end of 2027.

AI as a long-term growth driver

A study by BNP Paribas shows that artificial intelligence is expected to have a positive impact on economic growth. In the short term, however, the required investments may temporarily push inflation upwards.

"Over the longer term, AI will contribute to higher productivity and more efficient economic processes," says Koen De Leus, Chief Economist at BNP Paribas Fortis. "Our analysis shows that the positive growth effects of artificial intelligence, through increased productivity, will more than offset the negative effects of other long-term trends on GDP."

In the United States, this relates particularly to the impact of demographics, import tariffs, and energy prices. Thanks to AI, GDP is expected to be 3.61 percentage points higher by 2034 than in the baseline scenario, which does not consider the impact of AI. It should be noted, however, that there is enormous uncertainty about AI’s potential, with economists and AI experts giving estimates of its annual contribution to productivity growth that differ by a factor of 20.

In the eurozone, where the positive impact of defence spending is also considered alongside the aforementioned trends, the combined positive effect on GDP is expected to be 1.88 percentage points higher by 2034. The main reason for the smaller increase is that the impact of AI on the European economy is estimated to be significantly lower than in the United States. However, there is no full consensus on this assumption either.

The impact of AI on employment is expected to remain limited in the long term. While some jobs will disappear due to efficiency gains, others will be created through the emergence of new demand. Increased productivity and lower production costs will also make products more affordable. Therefore, jobs lost through efficiency gains are expected to be offset by increased demand for these lower-cost products.

Climate transition: short-term pain, long-term gain

The faster the transition is implemented, the higher GDP will be in the long term, as damage will be avoided. This is the conclusion of a study by Oxford Economics1. In the short term, however, an accelerated transition weighs on growth. Higher carbon pricing is intended to encourage consumers to reduce their consumption of carbon-intensive goods. This affects purchasing power and, consequently, consumption.

Oxford Economics’ Global Climate Service distinguishes between several potential transition scenarios. In each scenario, there is a trade-off between transition risk and physical risk.

The transition risk reflects the potential losses and damage associated with a rapid shift towards a lower-carbon, more environmentally sustainable economy aimed at limiting global warming. The substantial increase in carbon prices required for such a transition would push inflation higher in the short term and erode purchasing power.

However, over a somewhat longer horizon, there are significant cumulative economic gains compared with the current pace of action, as substantial climate-related damage is avoided. If we demonstrate real ambition, economic growth could accelerate further, as innovation breakthroughs would reduce future emissions-cutting costs while generating productivity gains. Additionally, the transition would create positive knowledge and innovation spillovers, open up new markets and industries, and provide greater certainty regarding strategic resources such as water and raw materials. By 2060, an accelerated net-zero transition could increase global GDP by 13 percentage points compared with a continuation of today's baseline scenario, which assumes a less ambitious climate strategy.

The longer the transition is delayed, the greater the physical risk. Extreme weather events become more frequent, resulting in significantly lower long-term GDP. Higher temperatures, particularly in countries that are already warm, reduce labour productivity and lead to a loss of output.

In the long term, the climate transition is expected to contribute to higher inflation, regardless of the scenario followed. “In each of the scenarios put forward by Oxford Economics, prices by 2050 are 20 percentage points higher than they would be at a 2% inflation rate. Inflation will therefore accelerate in any case,” says Koen De Leus. “The climate transition will put additional pressure on prices in the coming decades, and that is something we need to take into account.”

Belgium under pressure from public finances

As noted above, inflation is also rising in the short term. Combined with the structurally increasing term premium, which compensates long-term investors for growing geopolitical uncertainty, this is pushing long-term interest rates higher. Yields on 30-year Belgian government bonds are currently at, or close to, their highest level since 2012. In the United States and the United Kingdom, yields are approaching, or even exceeding, the levels seen in 2007 and 1998, respectively. Japan’s 30-year government bond yield is at its highest level since the bond was first issued in 1999.

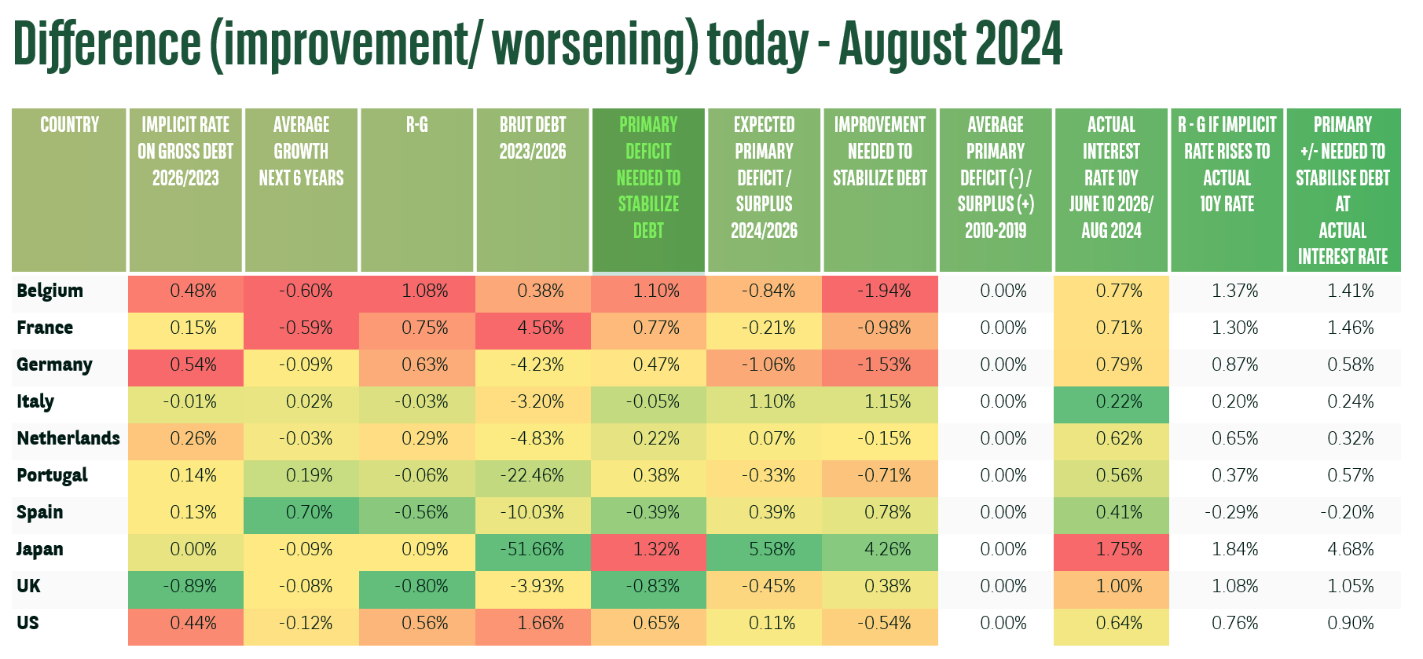

These developments have implications for the sustainability of high levels of public debt. The gap between expected nominal growth, which forms the denominator of the debt-to-GDP ratio, and the implicit interest rate on outstanding debt is narrowing. In Italy and the United Kingdom, the interest rate is already higher than the growth rate. Consequently, public debt (the numerator of the debt ratio) is rising faster than nominal GDP (the denominator). Even when the primary budget balance is in equilibrium and does not include interest payments, the debt ratio automatically increases. This increases the risk of a negative snowball effect. In order to stabilise public debt, these countries therefore need to achieve a primary surplus. Italy is succeeding in doing so. The United Kingdom is not.

Together with France, Belgium is also gradually moving into the danger zone, with expected nominal growth of less than one percentage point above the implicit interest rate. This rate is likely to increase in the coming years as governments refinance at today's higher interest rates. We do not expect long-term interest rates to decline. On the contrary. Given the current expected primary deficit of 3.5%, public debt as a percentage of GDP is set to continue rising. Stabilising the debt ratio would require an improvement of 3 percentage points.

Belgium, again alongside France, performs poorly when the evolution of key indicators between August 2024 and today is compared with 8 other major industrialised countries. Both countries are among the worst performers in terms of the increase in the implicit interest rate, gross public debt and primary deficit, and the decline in expected growth. In light of rising interest rates, this trend must be urgently reversed. Additional and challenging fiscal consolidation measures will be necessary.

Part II: financial markets

During this period of geopolitical turmoil, the world is searching for a new equilibrium. This creates uncertainty, but also perhaps even more opportunities.

“For those in any doubt, this is a Fourth Turning2,” says Philippe Gijsels, Chief Strategy Officer at BNP Paribas Fortis. “Politically, that means global instability, fragmentation and conflicts, whether armed or otherwise. One consequence of this is volatility: when equities, interest rates, commodities and currencies move, they tend to do so in large swings. As Koen De Leus and I explain in our book The New World Economy in 5 Trends 3, such a period is characterised by higher inflation and interest rates.”

AI: a K-shaped economy

So far, investors have largely been able to overlook the negative impact of global conflicts. Equity markets continue to perform relatively well. Artificial intelligence remains by far the dominant theme in financial markets. Following SpaceX's recent stock market listing, investors are now looking ahead to the expected listings of the other two giants, Anthropic and OpenAI. The construction of data centres to power AI applications requires substantial investment. While this is generating excellent financial results for technology companies, it is also creating high expectations. Some investors see parallels with the dot-com bubble of the late 1990s.

However, there is one important difference: the valuation of AI companies is supported by real and rapidly growing profits. Consequently, valuation metrics are more favourable than during the internet bubble. Nevertheless, questions remain about the sustainability of these AI-driven profits. Will investment in data centres continue at the current pace, accelerate further, or eventually come to a halt?

Against this backdrop, investors looking to gain exposure to AI should ideally invest in the broader ecosystem. Applications such as autonomous vehicles and robotics are expected to deliver significant efficiency gains and create new opportunities, as well as presenting new risks. The development of artificial intelligence is likely to benefit numerous themes and sectors, including healthcare, biotechnology and industry, through the productivity improvements it enables.

This is leading to the emergence of what is known as a 'K-shaped economy'. The share price trajectories of companies affected by the AI revolution increasingly resemble the letter K: the upward leg consists of stocks, themes and sectors that benefit from AI, while the downward leg consists of those perceived to be disadvantaged by it. Software development is a clear example, as it could come under pressure as AI’s programming capabilities continue to improve.

Commodities more strategic than ever

Gold is often regarded as an effective hedge against inflation and geopolitical uncertainty. However, it is not immune to the negative effects of sharply rising interest rates. The same applies to silver and, to a certain extent, industrial metals, which play a central role in the energy transition.

Philippe Gijsels explains: “That does not mean the greatest bull market in economic history, namely the commodities bull market, is over. Metals still have enormous potential. The sector has only just begun to invest again after more than 30 years of underinvestment. It will therefore take considerable time before supply can meet the rapidly growing demand. New developments, such as the blockade of the Strait of Hormuz and ongoing tensions between the United States and China, are also making energy and critical minerals, such as rare earth elements, more strategically important than ever.”

Equity markets

BNP Paribas Fortis remains optimistic about the long-term outlook for equity markets. Despite continued volatility, real assets are still a better option than cash in an inflationary environment.

In the shorter term, however, the bank is more cautious. Risks such as a deterioration in the situation in the Middle East, and the additional supply of shares resulting from the stock market listings of the aforementioned technology giants, may not yet be fully reflected in market valuations. Furthermore, many asset classes are likely to be under pressure from sharply rising long-term interest rates. This is particularly true for equities, especially growth stocks.

Bonds: in the belly of the curve

When it comes to bonds, BNP Paribas Fortis favours the 'belly of the curve'. In practice, this means a preference for bonds with maturities of between three and five years. Longer maturities are too vulnerable to rising interest rates, while short-term bond yields are too similar to cash returns.

Investors should also focus on high-quality bonds. Currently, credit spreads are at historically low levels, which do not provide sufficient compensation for the additional risks associated with lower-quality debt. BNP Paribas Fortis expects the US dollar to continue to weaken against many other currencies in the long term. For investors willing to take on additional risk, local-currency emerging market bonds may therefore be worth considering.

The coming years are likely to be economically challenging, with higher inflation, rising interest rates and geopolitical tensions demanding continued attention. At the same time, new growth opportunities are emerging for investors positioned to benefit from technological innovation, the sustainable transition, and high-quality investments.

Note: this text was written on 18 June 2026

1 https://www.oxfordeconomics.com/subscriptions/global-climate-service/#latestinsights

2 Howe, N. (2023). The Fourth Turning Is Here: What the Seasons of History Tell Us about How and When This Crisis Will End. India: Simon & Schuster. In this book, Howe argues that history unfolds in recurring cycles lasting between 80 and 100 years, divided into four distinct “turnings” or phases.

3 De Leus, K., & Gijsels, P. (2024). The New World Economy in 5 trends: Investing in times of superinflation, hyperinnovation & climate transition. Acc Publishing Group Ltd.

Gallery Koen De Leus & Philippe Gijsels