Invest Barometer: a new generation of investors emerges, driven by digital, crypto and the search for returns

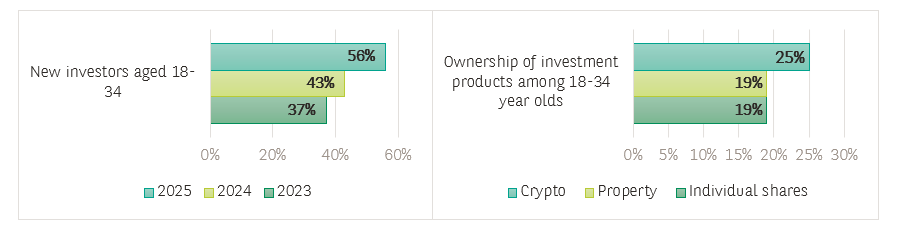

A wind of renewal is sweeping through the investment landscape in Belgium. According to the latest Invest Barometer conducted by Profacts in collaboration with BNP Paribas Fortis, the wave of new entrants is clearly young: 56% of new investors are aged between 18 and 34. More digitally connected and driven by performance, this generation is redefining expectations, perceptions of risk and what trust means in practice.

The world of investment is no longer the exclusive domain of experienced professionals. Financial markets are now attracting younger adults who are starting earlier, mainly through digital channels. According to the latest Invest Barometer1, over one in ten investors (12%, compared to 9% in 2024) reports having less than a year's experience. Among these newcomers, 56% are aged 18–34.

Cryptocurrency is the most popular asset class among young investors (25%), ahead of individual shares and property (Regulated real estate investment companies or FIIS/specialised real estate investment funds), which are both favoured by 19% of this group. Interestingly, 58% of 18–34-year-olds say they would prefer to buy cryptocurrencies through their bank, suggesting that they are seeking security and a framework, even for assets that are perceived as risky.

However, the core of the market remains structured around traditional products. The top three products across all age groups are investment funds (32%), Branch 23 insurance products (30%), and individual shares (29%). This hierarchy illustrates the importance of diversified portfolios and insurance-based solutions in Belgian financial culture. Yet the landscape is shifting : ETFs1 are gaining ground, rising to 16% (compared with 11% in 2024), reflecting a growing appetite for index-based management at controlled costs. Meanwhile, cryptocurrencies are rising to 13% (compared with 9% in 2024), becoming firmly established in the financial landscape beyond their initial speculative dimension. Nevertheless, a significant gap remains between awareness and actual adoption.

More immediate and pragmatic motivations

Young investors also stand out in terms of their motivations. They see investing as a means of accelerating their short- or medium-term life projects. Rather than exclusively building long-term wealth or saving for retirement, they invest to finance a trip, prepare a deposit for a home or support an entrepreneurial initiative. The search for immediate returns can partly be explained by the low interest rates on traditional savings accounts.

Frank Claus, Head of Investment Services Affluent & Private Banking : “Current generations reject passive delay, entering financial markets earlier while demanding full transparency on costs and performance metrics. Their focus extends beyond participation to a precise understanding of capital deployment. The fundamental transformation lies not in digital adoption, but in proactive financial ownership—with investors systematically shaping their economic futures at unprecedented stages.”

However, these dynamic faces several obstacles. Among non-investors attracted to the idea of investing, 48% cite a lack of financial knowledge as the main reason for not taking the step. The deficit in financial education remains a structural barrier. This is compounded by insufficient capital (44%) and a perception of excessive risk (37%). Moreover, 82% believe that they need to invest at least 100 euros per month, a misconception that creates a psychological barrier, even though accessible solutions exist from just a few dozen euros per month. These obstacles highlight the need for increased financial education and accessible information.

The central and evolving role of banks

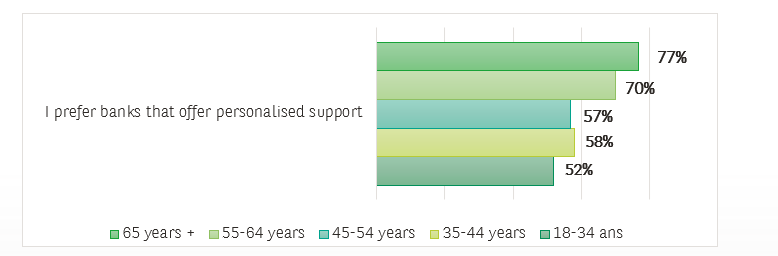

In this context, traditional banks continue to play a pivotal role: 63% of investors prefer to seek personalised advice from a bank. This preference is particularly strong among young people (52%) and those over 65 (77%).

Although digital platforms are appealing due to their competitive pricing and transparency, traditional banks must offer a high level of advice and responsiveness, as well as competitive pricing, to meet clients’ expectations of immediacy.

“While digital platforms provide investors with operational efficiency and control, market volatility underscores the need for structured guidance, emphasizes Frank Claus. The optimal approach combines self-directed decision-making with continuous access to rigorous portfolio management expertise.”

Social media and 'finfluencers' now play an important role in informing individuals. 49% of investors report being exposed to this type of content, a figure rising to 87% among 18–34-year-olds. However, visibility does not necessarily equate to credibility; only 28% of respondents trust this content, compared to 59% of 18–34-year-olds. This underlines the tension between the immediacy demanded by highly connected young people, the knowledge gap, and the need for reliable sources.

Financial institutions are therefore being called upon to invest further in education and accessible communication without compromising the quality of information provided. “The Invest Barometer 2025 does not indicate a sudden rupture, but rather a structural evolution,” concludes Frank Claus. In an environment characterized by information saturation and short-term market fluctuations, the critical advantage stems from methodical asset allocation. Enduring performance depends not on reactive speed, but on strategic portfolio architecture, systematic risk governance, and purpose-driven investment continuity.”

***

1 The Invest Barometer is an online survey conducted by Profacts. It was carried out in October and November 2025 among 1,286 adult investors, 278 potential investors, and 568 young investors aged 18 to 34.

2 An ETF (or “exchange-traded fund”) is an investment that seeks to track the performance of a stock market index.